Welcome, Educators. Your Retirement is Our Priority.

As a teacher, you dedicate your life to shaping the future. You deserve a retirement plan that honors that commitment. At Citizen Seguro, we specialize in helping educators like you navigate your 403(b), 457(b), pension options, and supplemental retirement strategies — so you can retire with dignity, security, and peace of mind.

Ready to Secure Your Retirement?

Schedule a free 30-minute consultation with a Citizen Seguro retirement specialist today.

01

403(b) Tax-Sheltered Annuity

The 403(b) is your primary tax-deferred savings vehicle as a school employee. We help you choose the right provider and investment options to maximize your contributions and grow your nest egg efficiently.

02

457(b) Deferred Compensation

Many school districts also offer a 457(b) plan as a powerful supplement to your 403(b). Unlike a 403(b), the 457(b) has no early withdrawal penalty, giving you even more flexibility in retirement. We’ll show you how to maximize both.

03

Pension & Supplemental Income

Your TRS or PERS pension is a great foundation, but it may not be enough on its own. We help you layer in supplemental income through annuities and LIRP strategies that fill the gap between your pension and your desired lifestyle in retirement.

You’ve Worked Hard for Your Future. Let’s Protect It Together.

Schedule your free, no-obligation retirement consultation today. We’ll review your current benefits, identify gaps, and build a personalized plan that gives you the retirement you truly deserve.

No pressure. No obligation. Just a friendly conversation about your future.

Understanding Your School District Retirement Options

Your Retirement Benefits — Explained

As a school district employee, you have access to two powerful tax-deferred retirement savings plans: the 403(b) and the 457(b). Together, these plans allow you to save significantly more than the private-sector average, reduce your taxable income today, and grow your nest egg tax-deferred for decades.

Most educators also receive a state pension (such as NYSTRS in New York), but that pension alone rarely replaces 100% of pre-retirement income. A well-structured 403(b), 457(b), and LIRP strategy fills that gap — giving you the retirement income you actually need.

At Citizen Seguro, we are authorized agents appointed with National Life Group, one of the country’s leading providers of school district retirement plans. We help you understand your options and build a personalized plan around your career and goals.

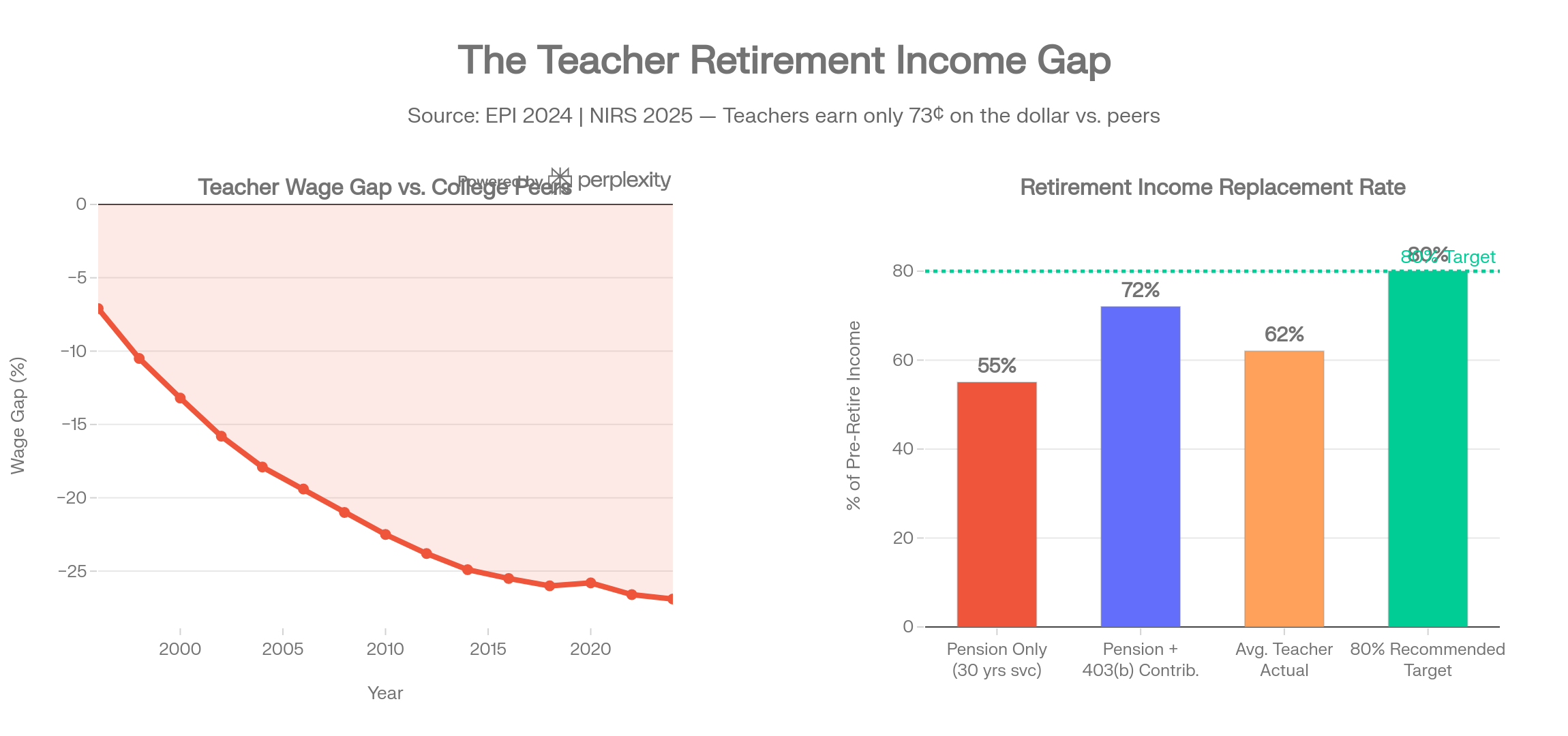

The Educator Income Gap: What the Numbers Tell You

Based on national data from the NEA, National Institute on Retirement Security, and Pew Charitable Trusts

NEA, 2025

Pew Charitable Trusts, 2021

Pew Research, 2025

The Hidden Cost of a Teaching Career

Teachers earn only 73¢ on the dollar vs. college-educated peers — and that wage penalty directly shrinks your pension and your savings. Here’s what the data shows.

Source: Economic Policy Institute 2024 • National Institute on Retirement Security 2025

© Citizen Seguro — Retirement Planning Specialists for Educators